The Q4 2025 broadband subscriber tally clarifies who owns the pipes feeding American homes, but it tells only half the story for multifamily.

The same operators that dominate the national rankings occupy a far more ambiguous position within apartment buildings, where specialized managed service providers (MSPs) continue to win business that national carriers cannot serve efficiently.

Maravedis’ U.S. Multifamily Rental Connectivity Market Analysis 2026-2031 tracks this divergence in the market-rate segment, and it is the data foundation for the analysis below. Understanding both sides of the carrier-MSP divide matters more than ever as merger activity reshapes the top of the market and state-level policy debates redefine the rules for bulk connectivity.

The Top 10 US Fixed Broadband Operators at Q4 2025

Based on the most recent reported quarterly figures, with some positions reflecting very recent M&A activity, the current ranking of US fixed broadband operators is as follows. This list follows standard industry convention by including fixed wireless access (FWA) in “fixed broadband,” because that is how the market is currently competing.

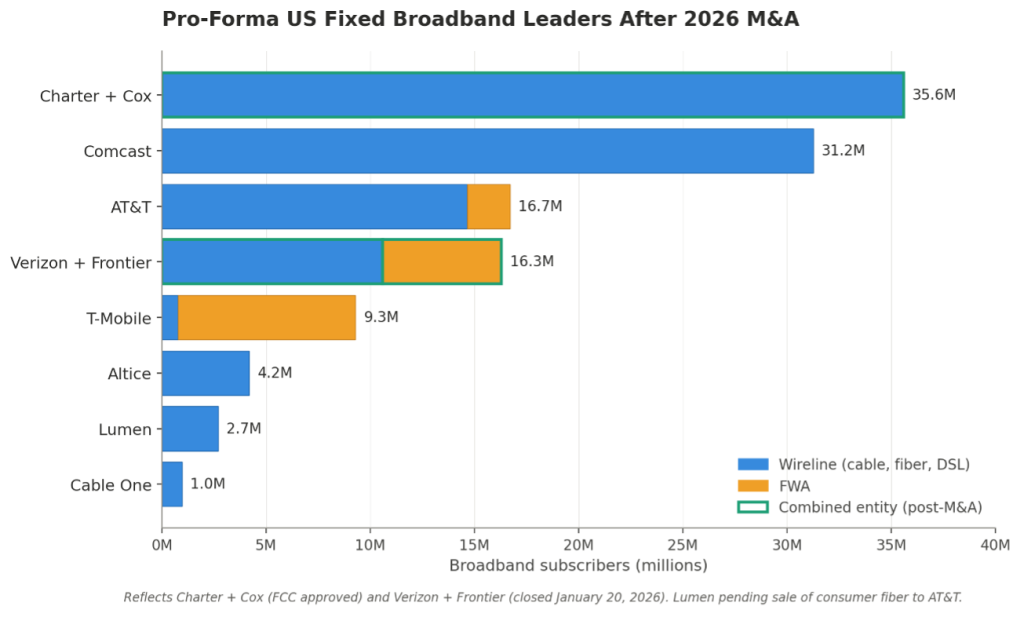

Comcast (Xfinity) leads with 31.25 million domestic broadband customers at the end of Q4 2025, comprising 28.71 million residential and 2.53 million business. Charter (Spectrum) follows at 29.7 million internet customers as of December 31, 2025. AT&T reports roughly 16.7 million consumer broadband subscribers, combining 10.4 million fiber, 2.04 million Internet Air FWA (1.49 million residential, 543,000 business), and 4.29 million non-fiber.

Verizon has approximately 13 million broadband connections, including over 5.7 million FWA subscribers and 7.32 million Fios internet customers; the combined Verizon-Frontier footprint reaches over 16.3 million connections following the close of the Frontier deal on January 20, 2026.

Recent industry data indicates that at the end of Q3 2025, top cable providers held about a 62.5% share of US broadband subscribers, a share that continues to erode as FWA and telco fibre capture net additions.

The 2026 Reshuffle

Two deals rewrite the leaderboard in 2026. Charter + Cox becomes the new number-one US broadband operator, with roughly 35.6 to 38 million subscribers, depending on whether business customers are included, displacing Comcast at the top.

Verizon + Frontier pushes Verizon’s combined fibre and FWA footprint to approximately 16.3 million connections, solidifying a clear number-three position behind the two cable giants.

For Multi-Dwelling Unit (MDU) owners, the consolidation matters less for the headline subscriber counts and more for the concentration of retail sales pressure. Fewer, larger carriers with bigger fibre footprints will increasingly push multi-gig bulk offers directly to property owners, and that dynamic is already shaping negotiations at the NMHC Top 50 level.

The Next Tier of Regional Operators

Below the top ten sits a cluster of regional cable operators that matter disproportionately for MDU but are less visible in headline rankings because most are now privately held and no longer report quarterly subscriber counts.

Mediacom serves roughly an estimated 1.4 to 1.5 million broadband residential subscribers across 22 states, with a focus on smaller Midwestern and Southeastern markets and a public commitment to multi-gig symmetrical service across one million homes by the end of 2026.

Astound Broadband, the sixth-largest cable MSO by footprint, serves over one million customers through the unified RCN, Grande, Wave, and enTouch networks, with a strong presence in dense urban markets including New York City, Chicago, Washington DC, Boston, Philadelphia, and the San Francisco Bay Area.

Breezeline, owned by Canada’s Cogeco, has just under 1 million total customers across broadband, video, and voice in 13 states. Midco operates roughly 500,000 subscribers in Kansas, Minnesota, North Dakota, South Dakota, and Wisconsin, including recent fiber expansion through the SCI Broadband acquisition.

WOW! (WideOpenWest), recently taken private in a $1.5 billion deal by DigitalBridge and Crestview Partners that closed on December 31, 2025, reports about 457,000 broadband subscribers with active fibre greenfield expansion in Central Florida, South Carolina, and Michigan. Some of these numbers are estimations, given that not all operators report their numbers.

These operators collectively serve several million MDU units and are often the primary retail incumbent in the buildings they pass. Their strategic postures vary, but most are now actively reorienting from legacy cable to fibre and are making the same strategic choice that the national carriers face: whether to engage MDUs through a generic retail motion or to build or acquire a dedicated managed Wi-Fi capability.

The FWA Caveat for MDU

The rankings above matter for market-share conversations, but they are not a map of who controls connectivity inside apartment buildings.

Strip out FWA and limit the view to wireline (cable, fiber, DSL), and the picture shifts. T-Mobile drops out almost entirely, the FWA portions of AT&T and Verizon shrink substantially, and Cox, Altice, Frontier, and Lumen move up the ranking.

For MDU-focused analysis, the wireline-only view is usually more relevant because FWA penetration in managed multifamily properties remains comparatively low. The Maravedis multifamily rental connectivity forecast segments penetration by building age and property size, and the data consistently shows that fibre-fed managed Wi-Fi outperforms FWA in larger, denser apartment communities, while FWA retains a second-line role in lower-density suburban properties.

How the Largest Operators Show Up Inside the Building

The biggest names at the national level play very different roles inside MDU. Comcast Xfinity Communities and AT&T Connected Communities have historically dominated bulk video and bulk internet placements in conventional multifamily, relying on network reach, brand familiarity, and, in some cases, upfront door fees to secure multi-year contracts.

Door fees transfer long-term value away from property owners in exchange for short-term cash. Revenue-share arrangements, where available, typically produce better long-term economics and warrant serious consideration before an owner signs a door-fee-based deal.

Verizon’s Fios wholesale and retail presence in MDU has always been concentrated in its Northeast and Mid-Atlantic footprint, and the Frontier acquisition extends that reach substantially into Texas, Florida, California, and other Frontier fibre markets. T-Mobile’s MDU relevance through FWA has been limited, but the Metronet fibre acquisition gives T-Mobile a greenfield and retrofit fibre platform that will gradually extend into managed multifamily deployments.

Cox has long served MDU with bulk cable and broadband, but will be absorbed into the Charter footprint. Altice retains an Optimum-branded MDU presence in its Northeast footprint, though it has been a net share loser to Verizon Fios and T-Mobile FWA in recent quarters.

For property owners, the key point is that large-operator MDU engagement tends to be transactional rather than operational. These carriers sell circuits, sometimes bulk, sometimes retail, and rarely take responsibility for property-wide Wi-Fi performance, PropTech integration, or resident support at the building level. That operational gap is where MSPs have built their businesses.

Where Smaller MSPs Win

Specialized MSPs compete by doing what national carriers are structurally unable to do. The core proposition is single-provider accountability for a property-wide network: one call center, one support team, one bill, and one point of contact for the property owner.

Operators such as Dojo Networks, Gigstreem, Elauwit, Mereo Fiber, Pavlov Media, and Zentro consolidate what would otherwise be three to five overlapping ISP circuits into a managed network designed for the building, not the household.

Many of these operators, alongside equipment vendors and property owners advancing the managed Wi-Fi model, are recognised annually through the Maravedis MDU Connectivity Awards, which are led by an independent panel of judges drawn from the top ranks of the sector, including property owners.

The resulting NOI case is increasingly quantifiable. Elauwit, for example, claims a 200- to 300-basis-point NOI lift for properties through consistent per-unit revenue and reduced operating costs from eliminating duplicative circuits and vendor touchpoints.

Roughly nine out of ten new multifamily development projects are choosing managed Wi-Fi over retail ISP models, according to operator commentary, and brownfield conversion from legacy retail to managed Wi-Fi has become one of the largest growth opportunities for independent MSPs.

The Maravedis 2026-2031 forecast sizes the managed Wi-Fi and bulk internet TAM across four property segments (building age crossed with property size) and projects continued penetration gains through 2031, with the fastest growth in newer large-format properties and Sun Belt build-to-rent communities.

The managed Wi-Fi value proposition rests on four advantages that retail carriers cannot match at scale: instant-on connectivity from lease signing, property-wide roaming with no unit-level equipment, the network as a backbone for PropTech and smart-building systems, and professional RF spectrum management that eliminates interference between units.

The forthcoming Maravedis PropTech Evolution in U.S. Multifamily, 2026–2031 report details how the managed network has become the operating layer for access control, HVAC, IoT, and smart-unit systems across the stack. Purpose-built platforms such as Calix SmartMDU illustrate how this convergence is being productized, bundling managed Wi-Fi, resident smart-home services, and PropTech integration into a single operating environment that MSPs, operators, and property owners can deploy across the property.

Scale in the MSP segment is measured in tens of thousands of units rather than millions. Zentro reports about 106,000 units. Elauwit serves more than 25,000 units across 25 states following its November 2025 IPO.

These are small numbers next to Comcast’s 31.25 million, but they translate into meaningful density inside the NMHC Top 50 portfolios, where the managed Wi-Fi conversation is not a subscriber conversation but a building-asset conversation.

The Competitive Pressure Point

The tension heading into 2026 is that the largest carriers are learning to sell bulk. Multi-gig bulk internet offers from AT&T, Verizon, Comcast, and Charter are increasingly targeted at national REITs and large ownership groups, often at price points that independent MSPs struggle to match on a raw Mbps-per-dollar basis.

Where big carriers still fall short is in service delivery, network operations inside the building, and PropTech integration. The question that will define the next two years is whether carriers can credibly extend their offering into managed Wi-Fi service delivery (organically or through acquisition), or whether MSPs will continue to hold the ground where the network ends at the unit door, and the resident experience begins.

Policy adds another variable. State-level legislation in California (AB 1414), Colorado, Massachusetts, and New York continues to challenge the bulk-billing model on which most independent MSPs’ economics depend.

These debates have too often centered narrowly on “consumer choice,” overlooking the cost efficiencies, access benefits, and productivity gains that professionally managed, community-wide networks deliver, particularly in affordable, student, and senior housing.

Maravedis is directly addressing that evidence gap through its Economic Impact Study of Bulk Managed Wi-Fi in U.S. Multifamily Housing, an in-progress research initiative quantifying the economic value of single-provider managed Wi-Fi for residents, property owners, service providers, and the broader economy.

If restrictive state actions succeed, the large carriers’ retail-direct model becomes relatively more advantaged. If they stall or are preempted at the federal level, as the FCC’s recent reversal on bulk billing effectively did, the managed Wi-Fi thesis strengthens, and with it the hybrid carrier-MSP arrangements that depend on property-wide participation economics.

The Bottom Line

The top ten US broadband operators own the long-haul and last-mile infrastructure that reaches every apartment building in the country, but subscriber count is not in control of the MDU opportunity.

Inside the property line, the competitive dynamic is fundamentally different. Large carriers are building internal MSP units and buying fiber platforms to close the operational gap; regional cable operators are acquiring managed Wi-Fi specialists to run as distinct MDU service lines; independent MSPs are leaning on carrier backhaul and equipment-vendor platforms to extend their reach and technology sophistication.

What remains durable for the independent segment is single-vendor accountability: one network owner, one support team, one contract that puts resident experience and PropTech integration on the hook.

For property owners focused on NOI and building asset value, that accountability model remains the structural advantage of the MSP segment, which is why a fragmented market of tens of thousands of buildings continues to resist the subscriber gravity of the national carriers, even as the lines between carriers and MSPs keep thinning.

For the full TAM forecast, segment-by-segment penetration model, MSP and equipment vendor profiles, and policy analysis underpinning this view, see the Maravedis U.S. Multifamily Rental Connectivity Market Analysis, 2026-2031; for the economic case supporting managed Wi-Fi in the current policy environment, the Maravedis Economic Impact Study of Bulk Managed Wi-Fi; and for the annual recognition of operators, vendors, and properties setting the benchmark in the segment, the Maravedis MDU Connectivity Awards.

For a forward look at how property technology is reshaping multifamily operations and the role of managed connectivity as the integration backbone, the forthcoming Maravedis PropTech Evolution in U.S. Multifamily, 2026–2031.

Article originally published here